By:- Dr. Prashant Thakur, Executive Director & Head – Research & Advisory, ANAROCK Group

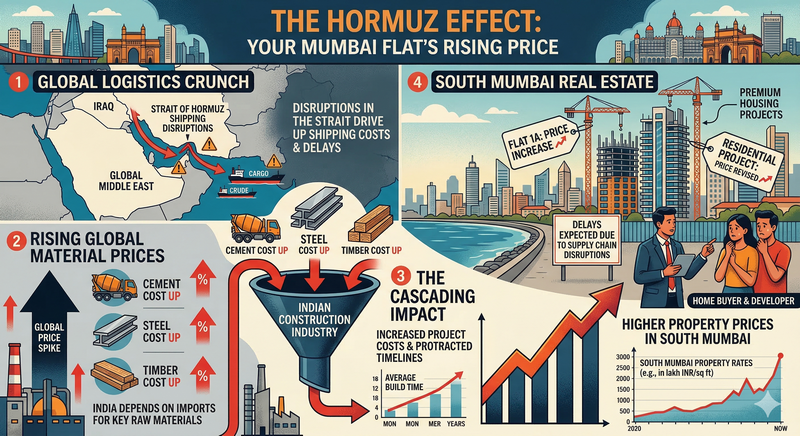

The proverbial Chinese curse “may you live in interesting times” is becoming manifest on the Indian real estate construction sector in ways few developers would have foreseen as they rang in 2026. The Strait of Hormuz blockade since early March 2026 has hit the sector hard with exploding material costs, supply delays – and potentially delayed and even stalled projects.

Iran’s stranglehold on this critical waterway between the Persian Gulf and the Gulf of Oman has impacted a substantial amount of India’s shipping imports. The forced reroutes of ships carrying construction materials around the Cape of Good Hope has added anywhere between 10-20 days to shipping times – and as much as and INR 1.5-3.5 lakh per container to the costs.

At a time when housing sales were already tapering, Indian developers are now confronted with an even starker landscape and must find new ways to weather the intensified storm. Diplomatic manoeuvring has succeeded in getting at least some LPG tanker ships through the Strait. However, bulk imports must now travel an additional 6000-10000 nautical miles, with marine fuel now at about INR 1 lakh/tonne. Also, there are additional ‘war surcharges’ and steeply hiked shipping insurance costs. It has become so serious that Indian regulators are now cracking down on shipping profiteering.

Construction Inputs Hit Hard

Steel prices have surged by around 20% to INR 72,000/tonne, from INR 62,000 earlier. At a very rough estimate, this adds approx. INR 50/sq. ft. to the cost of building high-rises in Mumbai, which currently has well over 10,000 luxury units under construction. The cost of hot rolled coil now hovers at INR 51,000-56,000 and may hit INR 62,000 by June if the situation does not change for the better.

Skyscrapers use ribbed steel rods embedded in concrete to give it tensile strength, and this added cost has a direct correlation to the cost and speed of constructing them. Diesel for construction cranes and mixers is heavily associated with the USD 100+ price of Brent crude. This price shock will reflect significantly on construction sites in Mumbai, Delhi-NCR, Hyderabad, and other high-rise-centric cities around the country.

With aluminium plants in Bahrain and Qatar now either partially or fully down, the price of aluminium – another important construction input – now hovers at around INR 3.5 lakh/tonne. Delhi’s facade-heavy office parks, where aluminium-glass curtain walls dominate the external envelope, will witness steep cost overruns. The price of bitumen, required to construct critical infrastructure projects like the Mumbai-Nashik expressways and Delhi’s peripheral roads, had already risen to INR 48,000-51,000/tonne.

Luxury housing is among the most affected segments. The Italian Statuario and Calacatta marble used in Mumbai’s sea-facing penthouses and other ultra-luxury units now comes with an addition INR 50-150/sq ft premium due to the rerouting fees, resulting in INR 6000/sq. ft. total all-in cost for this marble once it is installed. Premium plotted developments will face similar cost additions on imported fittings.

As it is, construction costs in cities Mumbai and Delhi have risen by as much as 39% over the past four years and now average at around INR 2,780/sq. ft. for mid-to-luxury skyscrapers. The cost of construction labour, which is commonly 25-35% of total project cost incurred by the developer, has risen by anywhere between 25-40% in the last 4-5 years because of sharpening skilled worker shortages and overall wage inflation.

Impact on Luxury Capital Mumbai

The impact will be most pronounced in India’s high-end housing hotspots. Mumbai Metropolitan Region (MMR), India’s skyscraper king with 300+ towers, over 5,500 high-rises, is also the leader in India’s ultra-luxury housing segment (homes priced above INR 40 Cr.). In 2024, India saw 59 ultra-luxury homes priced above INR 40 Cr. sell for a combined value of about INR 4,754 Cr., with Mumbai alone accounting for roughly 88% of both units and value in this bracket. Micro-markets such as Worli have emerged as epicentres: Worli by itself has logged over INR 5,500 Cr. of INR 40 Cr.-plus apartment sales in just two years and now accounts for about 40% of India’s ultra-luxury apartment transactions.

In volume terms, this speaks for the bulk of such high-end residential units sold across the country. South Mumbai, BKC, Worli, and Lower Parel lead the city’s luxury vertical boom and are where almost all such projects are heavily concentrated in Mumbai. These markets are going to experience the strongest blow of the Hormuz-induced construction price shocks. It will probably not impact ultra-luxury sales, though.

Luxury Sales – On Safer Ground (But Not Immune)

Buyers of affordable and mid-range housing continue to struggle with steep EMIs. The RBI has kept its key rate at 5.25%, so home loan interest rate is now between 7.35% and 13.20%, depending on various factors. Meanwhile, high oil prices due to the Gulf crisis are pushing up prices across the economy, so there is little hope of any rate cuts anytime soon. However, luxury housing sales do not really operate in that realm. While most developers of luxury projects expect to have to hike their prices by over 5%, their target clientele can largely absorb the hikes without much strain.

Then again, there is the matter of luxury housing sales to NRIs from the Gulf. These make up roughly 15-22% of high-end sales in cities like Mumbai and Delhi, according to industry estimates. Leading luxury developers state that NRIs contribute as much as 30% and above of their total sales value in premium and luxury projects. However, NRIs now face disrupted and delayed flight availability to India – among other things, to visit project sites and finalize property deals.

A Cloud Over 2026

Even if the Gulf war ends tomorrow, the Strait of Hormuz opens and shipping resumes normally, the additional real estate costs will not reduce immediately. We can expect a 2–8-week period for tanker pileups to clear as carriers test the safety of the route. Freight surcharges and higher shipping insurance will remain high in locked contracts. War‑risk surcharges and rerouting have cumulatively added anywhere between INR 2–3.5 lakh per container, especially for cargoes linked to Gulf routes. This severely impacts imported finishes, metals, and high‑value components commonly used in South Mumbai luxury towers. The port backlogs will delay the arrival of steel and aluminium.

A full reset will take anywhere between 1-3 months and certainly, a reboot of global shipping will not help developers to achieve their usual monsoon timelines. Much of the damage to 2026 is, so to say, cast in steel and concrete. In the meantime – if nothing else, the current turmoil is the clearest call for self-reliance that Indian real estate developers have ever heard.

Just as the ‘tariff war’ highlighted the need for India to find alternate markets to do business with, the Gulf war has revealed various previously unexamined, potentially weak links in the supply chain of construction materials. Certainly, the famous Indian ‘jugaad’ mindset will be called upon to the utmost in the times ahead.

Leave a Reply