LONDON/HOUSTON/SINGAPORE, 24

Imported LNG demand for power sector in Southeast Aisa and exposure to spot LNG in 2025

“While Southeast Asia is relatively insulated from immediate price shocks, the current crisis is a clear reminder of the region’s structural exposure to global fuel markets,” said Yanqi Cao, senior analyst, Asia Pacific power and renewable research at Wood Mackenzie. “Energy security is moving back to the top of the agenda, and this will have lasting implications for how power systems evolve in the region.”

Short-term impacts manageable, with uneven exposure

Rising gas and LNG prices are expected to feed into Southeast Asian power prices through Q2 2026, though impacts will remain manageable and vary significantly across markets.

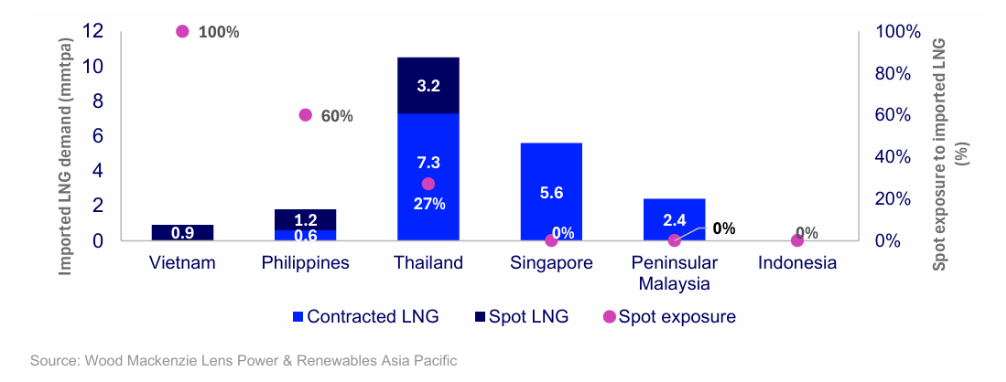

Singapore and the Philippines are likely to experience the earliest effects. Singapore’s wholesale electricity prices have increased by around 20% in the third week of March compared to pre-conflict levels, while prices in the Philippines are following similar trend over the same period. In both markets, price caps are expected to limit the impact on end consumers.

Elsewhere, regulatory mechanisms and subsidies will delay or dampen price increases. According to Wood Mackenzie, Thailand’s fuel tariff adjustment is not expected until May, while in Peninsular Malaysia, the impact is estimated at around a 1% increase in total power bills. Vietnam’s exposure remains limited, with gas accounting for just 9% of its power mix, and Indonesia’s fully subsidised tariff structure is expected to shield consumers from near-term changes.

Limited flexibility constrains fuel switching

If elevated fuel prices persist, most Southeast Asian markets will have limited ability to switch away from gas and LNG.

Vietnam and Indonesia may partially offset higher gas costs through increased coal generation and power imports. However, Singapore and Thailand where gas and LNG account for approximately 85% and 65% of generation capacity, respectively have more limited short-term alternatives. Malaysia and the Philippines also retain coal capacity, but plants are already operating near

Energy security concerns to accelerate structural shifts

Prolonged market disruption is likely to accelerate policy and investment shifts across the region, particularly in nuclear power and firmed renewable energy.

All six markets analysed have announced nuclear ambitions for 2030 – 2037, ranging from 1.2 GW in the Philippines to 4.0 – 6.4 GW in Vietnam. While these targets face execution challenges, heightened energy security concerns could drive renewed policy focus.

Firmed renewables combining wind and solar with battery storage are also emerging as a more scalable near-term solution. Policy momentum is building across the region, including higher tariff caps for hybrid projects in Vietnam, battery requirements for new renewables in the Philippines, storage auctions in Malaysia, and ambitious solar-plus-storage targets in Indonesia. Singapore is also advancing plans to import up to 6 GW of low-carbon electricity by 2035.

“Southeast Asia’s power markets are relatively well insulated from immediate shocks due to existing contractual and regulatory structures,” concluded Cao. “However, sustained volatility in global energy markets is likely to sharpen the region’s focus on energy security, accelerating investment in nuclear and firmed renewable capacity as alternatives to gas-fired generation.”

Leave a Reply